I Asked My Parents for Help

A tale of debt, taboo, humility, & life

Note: This article has been a long time coming. I had the idea to write it about a year ago, yet it was really hard to write and publish due to shame. I’m glad I can now give it to you.

There’s a taboo in our culture against asking for help.

When we turn 18, we’re expected by many to be “out on our ass” and fending for ourselves.

There is a strong emphasis on individualism, independence, and self-reliance.

I deeply internalized this expectation, and from the time I turned 18 in 2009, I asked my parents for very little. They continued to pay my phone bill and car insurance for 4 years during university, if I recall correctly, but apart from that, I was on my own.

I paid my way through college (with the help of a full academic scholarship), and for about 13 years, I fended for myself in the world. Paid my own way. Worked for a living. In 2015 I quit my last day job and started working full-time as an online creator and digital nomad.

I prided myself on my self-reliance. And I still do. I’m deeply stubborn on one level. I don’t like relying on others. I have a strong lone-wolf tendency — likely deriving from some kind of deep early-childhood wound that makes me feel I cannot depend on others for meeting my safety and security needs.

But, Last Year I Broke My Pattern…

As I’ve publicly shared, last year I experienced something of a financial implosion — and/or a deep ‘karmic reset’ around money, depending how you look at it.

It all started when I gave away about $10,000. I had a huge heart-opening experience and decided to cancel all debts people owed to me, cancel all subscriptions people were paying for my services, and send thousands of dollars in gifts via PayPal to various family and friends. It felt good and I believe it needed to happen.

Then, shortly after doing that, the crypto market—where most of my remaining savings were invested—crashed much worse than it already had. Then I suddenly found myself struggling to find new clients. And just like that, I started to go into survival mode. I had given away basically all my available liquidity, and I knew it would be foolish to touch my (now-fairly-small-five-figure) crypto nest egg during a bear market.

So I found myself spiraling rapidly into five-figure credit card debt. At the time, Tanja, Lila, and I were living on a volcanic island called Sao Miguel in the Azores, literally in the middle of the Atlantic Ocean. This turned out to be the scene for one of the most intense months-long ‘dark night’ periods of my life.

Quite ironic, considering we had been fantasizing about the Azores being a ‘New Earth Mecca’ where we were being ‘guided’ to find our dream home and community.

Life had other ideas.

The Azores chapter was more like an underworld journey for me. Isolated with my fiancé and our newborn baby on a tiny volcanic island in the middle of the Atlantic, knowing virtually no one, spiraling into debt, I was *triggered*.

So much deep shame and rage and grief and early-childhood wounding began erupting to the surface. So many intense purge and release processes, one of which involved all of us getting a nasty bout of Covid. Not to mention apparent encounters with dark spirits. Phew. It was a doozy.

We would’ve left Azores after 3-4 weeks, but in my inflated over-confidence about the islands, I had encouraged my family to book a trip to come see us—*before we had even reached the islands and experienced what they’re actually like.* My family had booked a trip several months into the future, and so destiny had us pegged: It was meant to be a 4-month initiation on a remote volcanic island.

Now, I should note that the islands *did* have gorgeous waterfalls and nature and lakes and hot springs and a few great restaurants and spas. It wasn’t all bad. It never is, right? Always a mixed bag. And of course the underworld initiation itself had some tremendous gifts to give me, not least of which was a substantial humbling. But damn, yeah, that was a messy time.

Back to the Money Story

Anywho, all of that is context for understanding how I managed to rack up about ~$25,000-$30,000 in (credit card) debt in 2022. I still had my low-5-figure mostly-crypto nest egg of investments that I didn’t want to touch. So, totaling my assets, I was about $15,000-$18,000 ‘in the red’ at the lowest point.

That was about the time I decided to swallow my pride and ask my parents for help. They had already given me a $9,000 loan some months earlier to help me avoid paying so much interest on the credit card debts. So, a few weeks before Christmas of 2022, I decided to ask them if they’d consider forgiving the loan as a Christmas gift. They generously agreed, and this was a huge weight off my back at that time.

A further surprise was that my partner Tanja, inspired by my parents’ generosity, decided to forgive the $3,000 I owed her at that time. We had been sharing expenses ~50/50 (and we still are doing so today), and I had fallen behind on paying her back. This was seriously unlike me and the last thing I ever wanted to do to her, yet it happened. She generously forgave the $3,000, and another large weight was lifted. (This was sort of a ‘karmic full circle’ moment, as I had once forgiven a ~$3,000 debt owed to me by an ex-girlfriend, and I now understood what it felt like to be on the other side of the fence.)

Nonetheless, this still left me with about ~$16,400 of remaining credit card debt to pay back. Thankfully, my financially savvy uncle instructed me to consolidate my debt onto several zero-percent-interest credit cards; I learned that if your credit score is decent, you can do ‘balance transfers’ and move your debt to new cards that will charge you 0% interest for 18-21 months. In this way I cut my interest costs to zero. Still, the $16,400 wasn’t going to pay itself off.

So, I dug in. I got super frugal, cutting all superfluous spending. Tanja and I moved in with her mother for a while—where we paid a modest rent, which helped us save and also created precious family time for us, Tanja’s mother, and our daughter. And I doubled down on rebuilding my business, going back to first principles and rebuilding from a foundation of deep loving service.

I believe that part of why I needed to go through this giant ‘karmic reset’ around money was that in previous years I had become inflated, ungrounded, and in some cases had begun over-charging for my services without delivering commensurate value to justify the price tag. This needed to be corrected.

So, as I focused on rebuilding, I endeavored to err on the side of *under-charging* for my services, and *over-delivering* on value. I also focused on building *ongoing* transformational containers that could support people long-term and thereby provide predictable recurring monthly income in an ongoing fashion. These decisions have worked out well so far, and a few months later I’ve finally begun to feel a sense of momentum again in the work that I do—plus a rewarding sense of truly showing up in deep service for those who choose to work with me.

In the past 7 months or so, I have paid off $12,400 of the remaining debt. Barring unforeseen disaster, I will pay off the remaining $3,999 about ~1.5 weeks from now. At that point, I will once again be debt-free, with iron-willed intent to never take on ‘bad debt’ again. I will have single-handedly paid off $16,400 in debt in about 7 months. Thank Heavens!

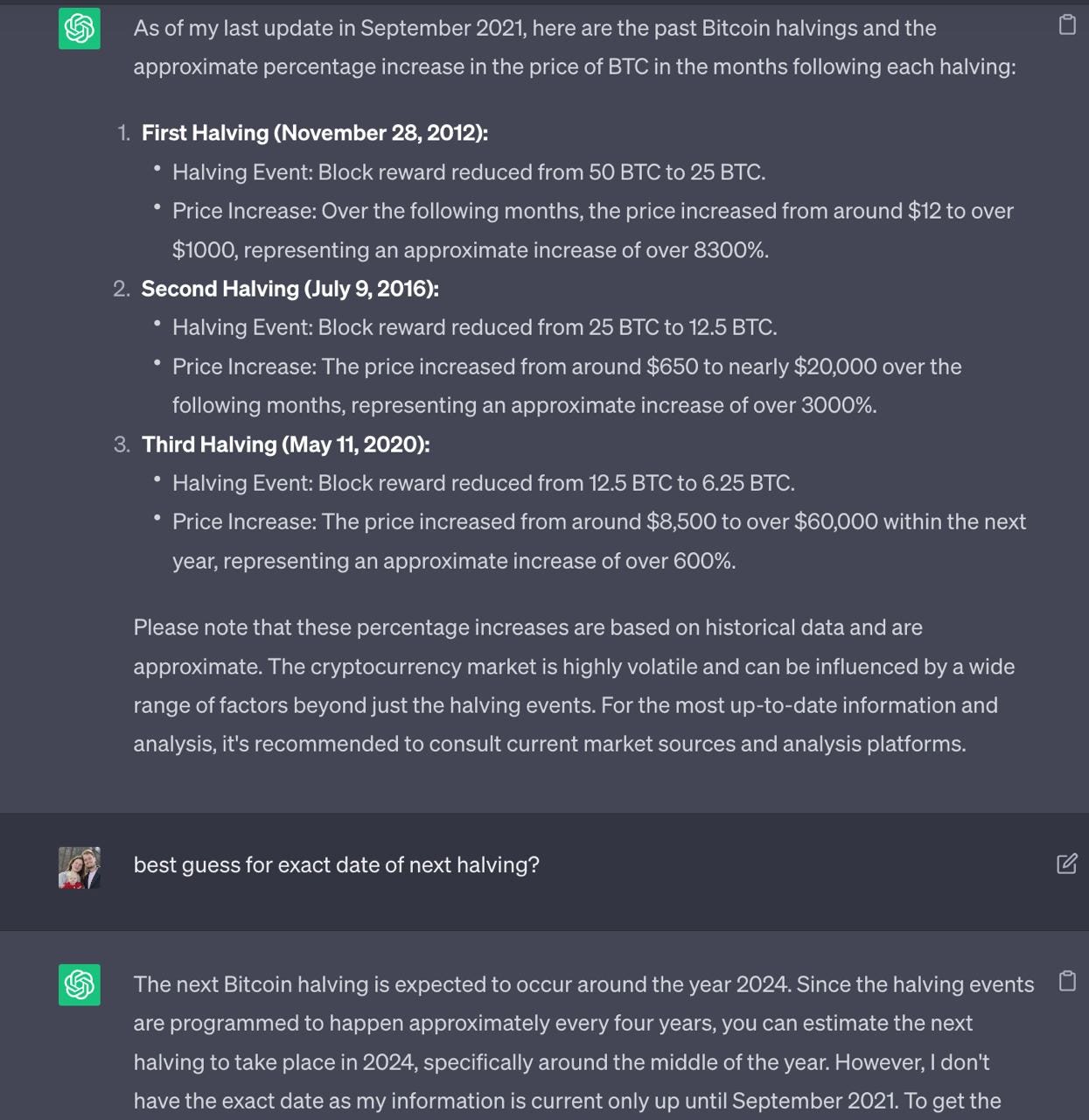

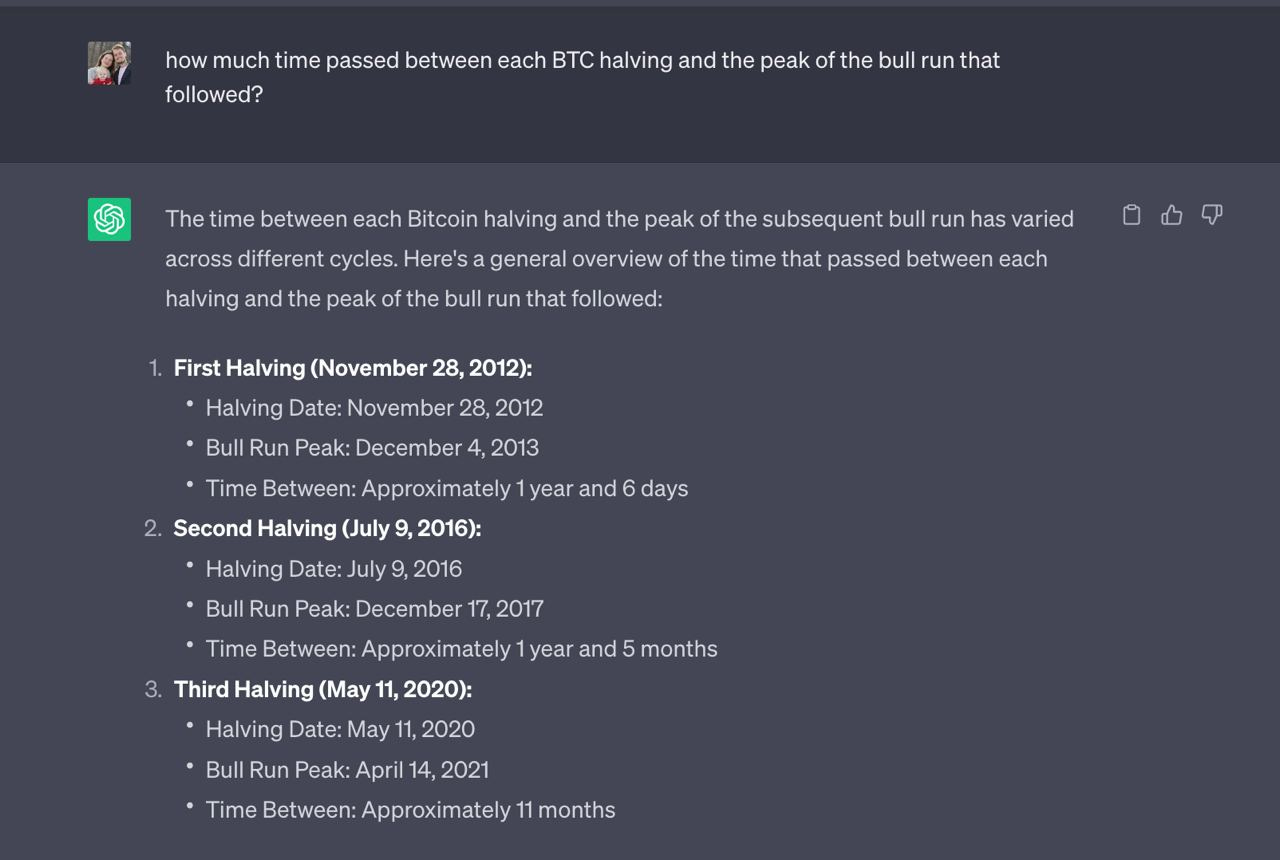

I will also have my growing 5-figure nest egg of savings/investments, which I plan to systematically grow and build in the coming months and years. The upcoming Bitcoin ‘halvening’ in 2024 is likely to be coupled with a crypto bull market, so I am planning for the best way to capitalize on this and withdraw most of my funds prior to the inevitable crash on the other side. I’ve now lived through two big crashes of the rollercoaster crypto market, I have felt the raw pain in my body, and I am ready to make wiser decisions next time.

Here are some screenshots showing why I believe there will be a post-halvening bull run and also outlining my strategy for systematically withdrawing my funds from the crypto market:

My first priority once the debt is paid off will be to save up a 6-month buffer of cash savings that could cover our family’s expenses for 6 months if need be. I currently plan to keep most of this cash in a wise.com USD account, which pays 4.3% annual interest. I am excited to wisely position our wealth to work for us and compound over time.

I will continue to invest in crypto, yet I currently feel I don’t want crypto investments to account for more than ~20-30% of our portfolio long-term.

In Sum

I’m proud of myself for doing whatever it took to pay off the remaining $16.4k of debt these past 7 months.

And I’m also proud of myself for finding the humility to ask my parents for help when I truly needed it, and also to accept the gift from Tanja when she offered it.

Asking for help is a truly humbling experience.

It can be very hard to do.

Nearly 12 months later, I’m still feeling some level of resistance around it.

I still wonder if I should’ve just ‘sucked it up,’ not accepted help, and found a way to pay off the full sum of debt by myself.

At the end of the day, though, I don’t think that’s true.

I’ve fended for myself for so long in my adult life. I am stubbornly, pridefully resistant to asking for help.

I sense that my soul was overdue for an experience of asking for and accepting help, and letting myself be supported.

It wasn’t easy, though, and truthfully I’m not in a hurry to ask for that level of help again. If I have to, I will, but I’m proactively doing what I can to avoid needing to do so.

Because while it’s important to know how to ask for help, there’s also a fine line there. If you find yourself regularly asking/allowing others to take responsibility for your life and your decisions, this might indicate a shadow that needs to be addressed.

At the same time, it’s also true that interdependence is our reality. No one is truly independent. And with a global economy that is increasingly in the shitter, I imagine that millions of people are presently finding themselves needing to ask for help in ways they aren’t fully comfortable with. Moving back in with one’s parents for periods of time—or never moving out in the first place—will probably become much more common in the West in the coming years/decades. It’s been a normal occurrence in the ‘developing world’ for centuries, where familial/tribal interdependence was never forgotten. The myth of the ‘independent, self-made man’ will likely continue to crumble in the West.

Living with our parents is probably not likely to be a long-term thing for our little family. With my end of the finances now recovered, and Tanja applying for various university jobs around the world, we’re fairly likely to move sometime soon.

Let’s see.

For now, I’m just ridiculously grateful to be debt-free again in a few days.

I’m finishing writing this article in the jungle at Kumankaya right now on retreat with Apotheosis, and there have been some incredible signs here that the financial tides are truly turning for my family and I.

That’s a good feeling.

I believe that through this experience of debt, I came to a much deeper understanding of the financial hardships many people on Earth are facing, and I solidified a rock-solid discipline & long-term-planning capacity that ought to serve me well as a wealth builder.

Presently it really feels like this is just the beginning.

At age 32, I feel like a newborn baby, and I’m ready to play.

Let’s dance.

It’s time to wholeheartedly choose a higher financial paradigm.

It’s time to create.

Let’s go.

Love,

J

P.S. Wild Freedom is happening in a little less than 4 weeks. Still time to join us if you act soon.

Jordan Bates is the author of Both, Neither, Far Beyond Either and other books.